Australia’s cost of living has reached a breaking point. Safe, affordable homes are slipping further out of reach for everyday Australians, placing pressure on families, workers and communities across the country.

If our government fails to act now, this housing shortfall will continue to pull people out of the workforce, overwhelm essential services and undermine the quality of life we’ve worked so hard to build.

With a federal election approaching and over 940,000 households set to require accommodation by 2041, the need for long-term solutions is more vital than ever.

That’s why Home In Place is calling on the government to build one in every ten new homes nationwide.

Here, we’ll explore who Australia’s housing crisis affects, in what ways and how our One in Ten strategy offers a meaningful and sustainable solution. Discover why strong government leadership is essential, and what you can do to help restore Australia’s housing system.

What is the cost of living crisis?

Australia’s cost of living crisis refers to the sharp rise in everyday expenses like accommodation, groceries, utilities and fuel, as incomes struggle to keep pace. Driven largely by inflation and sustained high interest rates, this disparity places a serious strain on households across the country.

Today, many Australians are finding it increasingly difficult to cover necessities, let alone work towards home ownership. While ABS data shows wages increased by 3.2% in the 12 months to early 2025, this has failed to offset the rising cost of living essentials.

Dissatisfaction is especially high in New South Wales, where 90% of workers say their income no longer reflects the cost of living.

Housing is one of the most visible pressure points in this cost of living crisis. The average household now spends around 33% of its income on rent, up from 26% just five years ago.¹ Meanwhile, mortgage payments now consume 45% of a median household’s pre-tax income.¹ This increase means families are dedicating nearly twice as much of their income to staying housed.

As this financial pressure grows, more people are taking on extra work just to make ends meet. For instance, around 28% of surveyed adults aged 18 to 35 are working additional jobs or longer hours to manage rising costs.²

The long-term impact of this imbalance is deeply concerning. “If we froze house prices today, it would take 30 years for wages to catch up so that houses were affordable,” states Martin Kennedy, Group Executive Manager Marketing & Public Affairs at Home In Place.

Such stress is reshaping where people are choosing to live and work. According to recruitment firm Robert Walters, 54% of Australian workers are planning to move interstate in search of better pay or improved affordability.

Many others feel they need to leave the country altogether. Keep reading to learn more about the consequences of our housing crisis on the Exit Generation.

The Exit Generation: how Australia’s housing crisis impacts key workers

In September 2025, Home In Place surveyed over 1,000 individuals aged 18 to 35 to reveal their opinions on Australia’s housing crisis. This group includes many key workers, such as early childhood educators, hospitality staff, and teachers, who are essential to Australia’s economy.

The results paint a clear picture of how housing pressure is negatively impacting young Australians and point to a broader national risk.

Without significant improvements in housing supply and affordability, Australia could lose skilled workers to countries with more accessible pathways to secure housing.

Here, we highlight the survey’s key findings.

Moving overseas is attractive to many

More than half of young Australians (53%) report they would consider moving overseas for more affordable housing, and 16% state they definitely would.

Today, the choice to live abroad isn’t just about chasing adventure. It has become a practical response to growing financial pressure.

Young workers are looking for places where their income stretches further and where secure, reasonably priced housing is within reach.

In Australia, rental costs vary widely between cities and regions, but incomes for key workers sit within a narrow band. This means that those working in major health, education, hospitality, and entertainment precincts often face a difficult choice to pay high inner-city rents or endure long, costly commutes from areas they can afford.

Over time, these pressures accumulate. High living costs, limited housing options near job centres, and the ongoing strain of rental stress and transport expenses push many young people to rethink their future in Australia.

Moving overseas is appealing because it offers what they struggle to find locally: affordable housing, better work–life balance, and the chance to build long-term stability without sacrificing most of their earnings.

Home ownership feels out of reach

For many young Australians, buying a home no longer feels feasible, even in the far-off future. Only 20% say they are very likely to ever own property, while half remain unsure or pessimistic about their prospects.

This uncertainty is already shaping behaviour, with 19% having paused or abandoned their efforts to save for a deposit.

The reasons behind this shift are clear. Rising living costs and stagnant wages are eroding the financial foundations young people need to enter the market.

The survey identifies the most common barriers preventing home ownership today:

- 35.4% cannot save a deposit because high rents and everyday expenses absorb most of their income

- 20.4% believe mortgage repayments would be unmanageable even if they could purchase

- 12.1% lack the borrowing capacity required for a home loan

- 11.2% face job insecurity that makes long-term financial commitments risky

- 10.3% say the homes they can afford are located in areas that do not meet their needs

- 7.7% are restricted by existing personal debt

These obstacles compound over time, making the first step into the property market increasingly difficult. On average, saving a standard 20% deposit now takes nearly 12 years nationally, and more than a decade in Sydney, Adelaide, Brisbane, and Perth.¹

The challenge continues even after a deposit is secured. According to Domain data, as of February 2025, first-home buyers aged 25-34 who purchase an entry-level property need to allocate an average of 43% of after-tax income to mortgage repayments.

This level of financial strain reinforces why so many young Australians feel locked out of long-term housing security. Indeed, the share of renting households grew from 26% to 31% between 1995 and 2020, reflecting the increasing challenge of entering home ownership.³

Rental stress is at unsustainable levels

Rental stress is a harsh reality for many young Australians, with approximately half of survey participants spending 30% or more of their income on rent, and 27% spending over half.

Long-term data backs this trend. The Rental Affordability Index (2015–2025) shows affordability has fallen in most cities, impacting communities across the country.³

While conditions stabilised in 2025 in every capital except Perth and Brisbane, affordability remains far below pre-pandemic levels, and finding an affordable private rental is still a serious obstacle.

Regional Australia isn’t much better. In 2025, rental affordability fell by 1% to 5% throughout most regional areas, with many reporting their lowest affordability levels in the past two years.

Key workers tend to feel this burden the most. Fewer than 1% of rentals are affordable for an early childhood educator, 1.4% for a nurse, 0.8% for a hospitality worker, and only 2.2% for an ambulance officer.⁴

Let’s take a closer look at the root causes of this rental stress.

Why is rent so expensive in Australia?

Rent has become so expensive in Australia because more people are competing for fewer homes, and the system is making it harder for households to move out of renting and into ownership.

Investor incentives

For years, tax settings like negative gearing and the capital gains discount have encouraged property investment.

While this has increased investor activity, it has also pushed up property prices, making it harder for first-home buyers to compete.

Many people who would have once bought a home are now renting for longer, placing ongoing pressure on available rentals.

Rising interest rates

Rising interest rates since 2022 have also flowed directly through to renters. As mortgage repayments increased, many landlords raised rents to cover higher costs.

At the same time, higher construction costs slowed new housing projects, reducing the number of rental homes entering the market.

Limited supply

The closure of the National Rental Affordability Scheme (NRAS) plays a major role in the shortfall of affordable housing.

This scheme, introduced to encourage housing providers to offer lower-cost rentals to low-income households, stopped accepting new applicants in 2014 and will be fully phased out by 2026.

NRAS supported more than 38,000 affordable rental properties, and its wind-down has left a significant gap in the market.

With fewer feasible options available, more low- and very low-income Australians are being pushed into the private rental market and forced to pay rents that far exceed what they can afford.

Moreover, supply is being tightened by homes sitting empty in inner-city and holiday areas, where properties are held for future value or used for short-stay accommodation instead of long-term housing.

Natural disasters

Unfortunately, natural disasters like the 2020 bushfires and 2022 floods have made the situation even worse by damaging existing rental homes and delaying new developments, particularly in regional areas.

More competition for rentals

On top of this, competition within the rental market has intensified. With home ownership feeling increasingly out of reach, higher-income renters are often choosing more affordable homes while saving for a deposit.

This leaves fewer options for lower-income households and forces many into less secure housing, even when they are doing everything possible to stay afloat.

Life milestones are being pushed back

Increased costs are shifting the timelines Australians once envisioned for major life events.

According to the survey, 21% have delayed important milestones such as further study, moving out of home, or starting a family because they simply can’t afford the financial commitment.

These findings highlight how housing pressure isn’t just influencing where young people live now, but how and when they plan their futures.

Men and women may react differently to rising costs

Overall, 48% of young Australians have cut back on lifestyle spending, and 34% have reduced essential spending, including food, health care, or utilities.

Within this data, there are clear differences in how men and women respond to increasing living costs. Women are more likely to reduce their spending on essentials such as food, health care, and utilities, while men are more likely to take on extra work or additional hours to manage rising expenses.

These responses suggest that financial pressure is reshaping daily habits and wellbeing, with gender influencing the strategies young people use to cope.

There is public support for new social and affordable housing

The survey results show strong and rising public support for large-scale investment in social and affordable housing, underlining the urgency for long-term policy reform.

Nearly 80% of respondents believe it is important for the government to build more social and affordable housing, and 46% say it is very important.

It’s clear that young Australians are calling for a housing system that puts people first and gives every community and individual a fair chance to thrive.

Disappointment in the government’s lack of action

Australians want concrete measures to be taken, expecting governments to rebuild a housing system that people can actually live in.

Yet, 55% of respondents believe that the government isn’t doing enough to help young people secure housing.

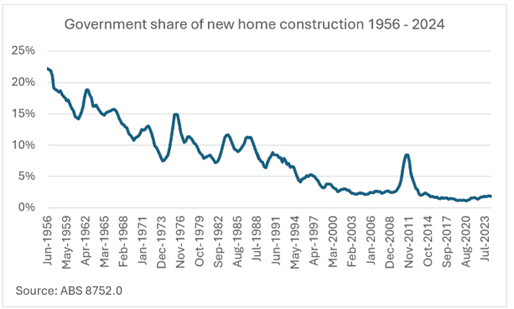

“In the 50s and 60s, governments built around 15% of all new homes. In the 70s and 80s, they were still building 10% of all new homes. These days, they barely build 2%,” Mr Kennedy reports.

The above chart shows not just a reduction in government-built homes, but a deliberate handover of housing responsibility from the public sector to private developers. This shift has removed one of Australia’s most critical affordability safeguards.

When governments stopped building homes at scale, Australia lost more than supply; it lost a stabilising force that once helped balance market pressures.

Without this anchor, affordability is now shaped almost entirely by private sector drivers such as land values, construction costs, investor returns, and lending conditions. Homes are built when they are profitable, not necessarily when communities need them.

As construction costs rise or profit margins shrink, private investment slows, pushing prices and rents higher. With no strong public mechanism to absorb these shocks, households are left exposed to forces they can’t control.

explains Mr Kennedy.“When a market can’t provide something essential like housing at a price regular people can afford, then it has failed, and it’s time for the government to step in,”

How the Housing Australia Future Fund can help

Established in 2023, the Housing Australia Future Fund (HAFF) has been a significant step forward in the fight against our housing crisis. This initiative provides up to $500M each year to help deliver 40,000 new social and affordable homes.

At its core, the HAFF makes affordable housing financially viable by supporting construction and long-term management, especially when rents need to remain below market levels.

Its yearly payments help Community Housing Providers to partner with developers, investors and government teams. By combining financial backing with land, tenancy services and housing management expertise, it’s easier to bring new affordable housing projects to life.

This funding eases financial pressure for tenants, too. Living in a HAFF-supported home can cut annual housing costs by an average of $9,500 compared to an equivalent private rental. Over 25 years, that equates to a total of $7.15B in cost-of-living savings and greater stability for thousands of households.5

The imminent third and largest round of HAFF funding offers an invaluable opportunity to deliver 21,000 more homes now, while strengthening the capacity of community housing providers like Home In Place to keep supporting those in need into the future.

‘These homes will deliver security and stability for tens of thousands of Australians, providing a solid foundation for health, education and employment,’ says Mark Degotardi, CEO of Australian Community Housing.

Equipped with this funding, the community housing sector is ready and mobilised to deliver at scale, with providers across Australia already working to provide new housing.

However, 21,000 homes won’t fulfil Australia’s affordable housing needs. Even a doubling or quadrupling of the HAFF would still fall short of transforming the market on its own.

A larger, long-term investment in non-market housing is essential. A strong and growing supply of social and affordable homes does more than help those directly housed. Over time, it can introduce real competition into the rental market, easing pressure on prices and improving affordability for all Australians.

Tackling Australia’s housing crisis with the One in Ten strategy

At Home In Place, we continue to leverage rigorous research and our tenants’ lived experiences to advocate for real change. We call for practical policy reform that creates fair, secure pathways into a stable home, not just temporary relief.

At the time of writing, government spending on housing sits at just 0.6% of the national budget. For decades, responsibility has been shifted to the private market to deliver homes people can actually afford.

The result has been a system that leaves too many Australians behind. When safe housing becomes unattainable, the impact reaches far beyond rent. It affects health, education, employment and community connection. Urgent action is needed to restore balance and protect the social stability we all rely on.

As Martin Kennedy highlights, ‘this is not about providing incentives to private builders, or offering subsidies to first home buyers – it’s about the government stepping up and taking the lead where the private sector can’t, or won’t.’

Our “One in Ten” campaign calls for the government to deliver one social or affordable housing development for every ten new homes built.

This clear, practical target can steadily increase supply, opening more doors to secure living for people who are struggling to call somewhere home.

Unlike short-term funding boosts, the One in Ten strategy demands a structural shift in how housing is delivered.

As mentioned above, the HAFF, while valuable, isn’t large enough to meet this level of need on its own. One in Ten goes further by embedding affordable housing into the fabric of future growth.

Instead of being limited to a fixed number of homes, it scales automatically with population growth and housing demand, ensuring social and affordable supply stays proportionate over time.

This commitment will ease pressure today while creating a fairer and more resilient housing system for generations to come.

Join our mission to make housing more affordable

Behind these Australian housing crisis statistics are real people cutting back on essentials, moving away from family, and living with constant uncertainty about whether they will be able to keep a roof over their heads.

At Home In Place, we believe that access to safe, secure and affordable housing is not only a basic human right but also a core government responsibility. To drive this duty, we’re calling for structural change, not just short-term fixes.

Our One in Ten strategy would rebuild a permanent public role in housing supply and create more pathways into stable housing for people who are currently locked out.

Please help us make this commitment a reality. Email your member of parliament, share this article with friends, family and colleagues, and start conversations about what a fair housing system should look like.

The more people who understand and support the One in Ten approach, the closer we come to building a brighter future for all Australians.

References

- Cotality 2025, Housing Affordability Report: Australia, RP Data Pty Ltd t/as Cotality, November.

- Home In Place 2025, The Exit Generation: Findings from the Home In Place Youth Housing Survey, September.

- SGS Economics & Planning 2025, Rental Affordability Index 2025, SGS Economics & Planning, November.

- Anglicare Australia 2024, Rental Affordability Snapshot: Essential Workers Report, 2nd edn, Anglicare Australia.

- Nygaard, CA & Salari, M 2025, Maximising Investment in Social and Affordable Housing in Australia: Estimating the Societal Benefits of Housing Australia Future Fund Supported Housing, PowerHousing Australia & Community Housing Industry Association, Canberra.